INNOVATION

Central banks are looking to the future. Let’s keep money safe, open and convenient for all

SEPTEMBER 8, 2020 | BY RAJ DHAMODHARAN

Even before the COVID-19 pandemic – and certainly since – data has shown that consumers are moving away from physical cash, and online commerce is accelerating rapidly. At the same time, we are seeing the continued development of privately issued cryptocurrencies based on blockchain and not backed by any central bank.

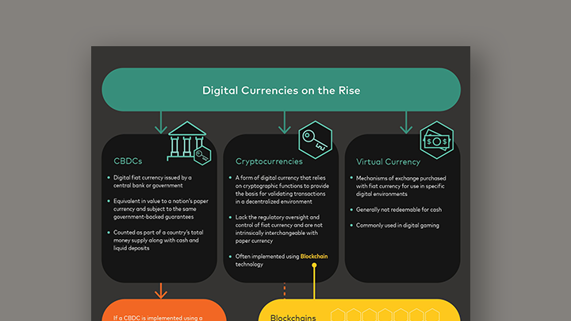

With the global economy racing to embrace digital, central banks also have their eye firmly on the future and how to support innovation, while keeping a grip on monetary policy and financial stability. Many have understandably accelerated their investigations into the possibility of digital fiat currencies issued by central banks and provided the same government-backed guarantees as a nation’s paper currency.

In fact, 80% of central banks are exploring central bank digital currencies (CBDCs) in some form, and 10% plan to roll out a digital currency within three years, according to a recent survey by the Bank for International Settlements. They are doing so for a variety of reasons: to modernize national payment systems, to deal with inefficiencies associated with the printing and movement of money, or to accelerate financial inclusion, particularly as cash is being used less and less.

China and the Bahamas have already rolled out pilots to better understand how a CBDC would work in practice. In France and Singapore, policymakers are looking into using CBDCs for wholesale transactions to help speed up the flow of bank-to-bank payments and streamline financial market operations. The United Kingdom and Sweden are both looking at the merits of CBDCs for retail banking. I expect more jurisdictions to do the same, and Mastercard is ready to support central banks as they evaluate these choices.

The best solutions are built with the customer at the center

CBDCs may offer an enticing value proposition in an increasingly digital world. But a change of such magnitude should be carefully stacked up against other innovative solutions, including those already in the pipeline that use existing technology and know-how to support many of the objectives central banks hope to realize through CBDCs.

For example, an effective and resilient real-time payment infrastructure can not only increase the speed of settlement, moving money faster and supporting productive economic activity, but can also be integrated with innovative new applications and services, such as auto-reconciliation for businesses and mobile payments for the unbanked. These are achievable with widely accepted, understood and interoperable technology, and can support the realization of a truly digital economy.

What is the best way to deliver this vision – where everyone can benefit from enhanced value, security, safety and scale? As with any innovation, the best solutions are built with customers at the center of the equation and that meet real needs. They need to integrate with existing infrastructure that consumers, banks and governments already trust.

Considering a new way of delivering money to the public will take time. If CBDCs are part of the future for some, then we will work with central banks to maintain and strengthen trust in the payment ecosystem by championing strong anti-money laundering standards, by protecting consumers and their data, and by delivering a level playing field for all. We will also help to ensure the critically needed interoperability between physical cash, bank deposits, and any future digital currency.

We believe that this is best done through partnerships between public and private sector. As a company that supports both card and account-to-account payments, we can help central banks as they look for solutions that are seamlessly integrated with all existing ways to pay. We can help assess what can be best achieved building on existing and emerging private sector infrastructure. And, along with like-minded institutions, we can shape the next generation of payments by working together on rules and standards through shared engagement with regulators and policymakers.

Together we can co-create value-added solutions that seek to strengthen our core principles of trust, privacy, and a great consumer experience, no matter how people want to pay. Mastercard has been investing in the development of technologies and tools to realize the vision of a digital currency that is open, secure and simple to use for consumers and business. We stand ready to collaborate with central banks and global institutions to realize this vision.

MASTERCARD SIGNALS

The rise of digital currencies

-

2020

- Central banks are looking to the future

Newsroom

Newsroom